Article

- why is your company struggling

Published

9 July 2020

Introduction

This is the second article in a series about turnaround management.

The first article is a general introduction to the turnaround management concept with overall recommendations for how to tackle turnaround situations, including learnings from the great financial crisis.

In this article, we will take a closer look at the diagnostic step of turnaround management. We will explain why this step is essential and provide you with inspiration for how it can be done.

Turnaround diagnostics

All businesses can experience rough times. However, if a business experiences declining, critical and/or non-sustainable financial results, it is in need of a turnaround in its performance.

Essentially, a turnaround is a massive short-term performance improvement in a constrained environment. But due to poor performance, a business in need of a turnaround will usually experience scarcity in excess time, resources and capital to invest to ensure a successful outcome of the turnaround. Therefore, the actions taken need to be very focused and very impactful.

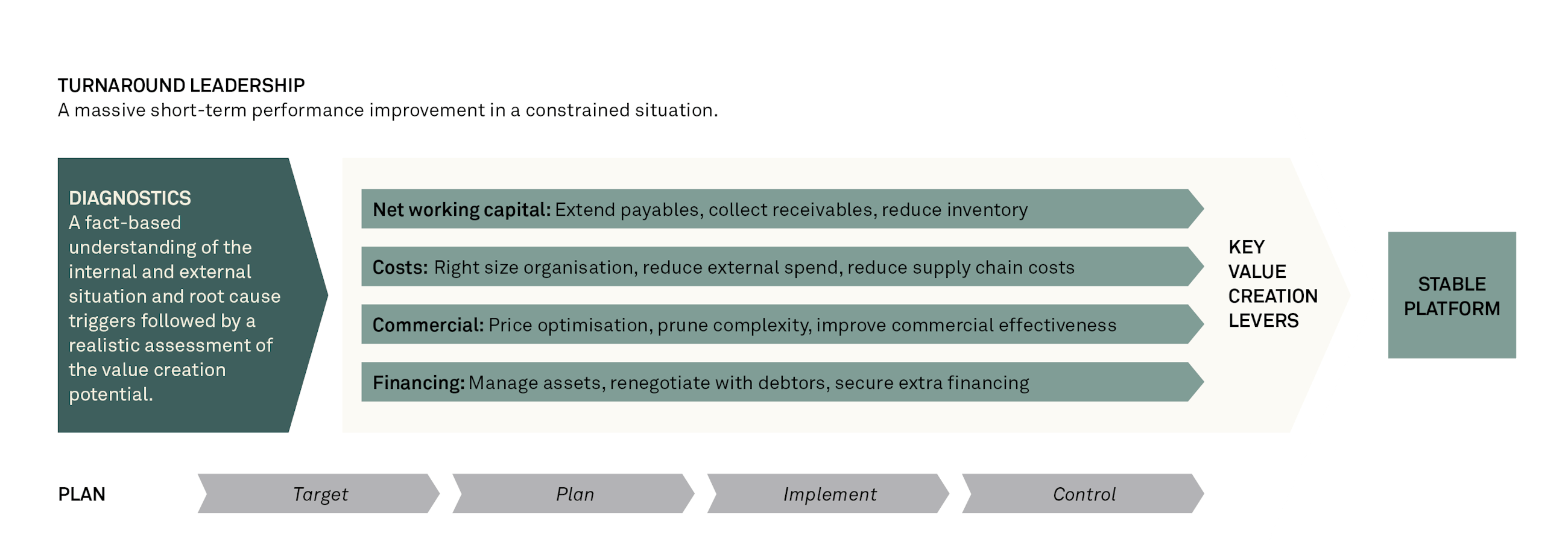

All cases are unique, and thus there is no magic formula for how to succeed in turnarounds. However, one of three critical requirements to succeed is diagnosing the current and future business situation from a cash flow perspective and developing a structured performance management and implementation approach to ensure needed performance improvements. This was outlined in the introductory article and is visualised in the turnaround toolkit below.

Figure 1: The turnaround toolkit

As part of the diagnostic effort, you should also evaluate the forward-looking cash flow, as this represents the summary of the expected impact of the ongoing business as well as turnaround actions. It can also indicate if there is a viable business going forward. We will touch more upon this subject in the section.

Diagnostics 2: the forward-looking cash flow.

Critical to succeed: The right diagnosis, a focused value creation plan and performance management

Going somewhere? Modern GPS technology can work wonders when it comes to finding a specific location. It will give you directions and even tailor them for your choice of transport. However, it needs to know one key piece of information in order to help you find your destination. It needs to know where your starting point is. In the same way, it is vital to know your starting point in a turnaround effort. To move forward, you must know where you are standing right now. To know this, you must perform diagnostics.

It is important that you understand the problem all the way down to the root causes if you want to solve the challenges with lasting impact. The best way to achieve this is by performing factual diagnostics.

By conducting thorough diagnostics, you reduce the risk and increase the chances of success.

If the situation is severe, and a turnaround situation is at hand, it is not sufficient to identify and try to fix one or a few leading indicators that are off track, e.g. sales challenges or the like. This may be only one of many problems, and therefore you must perform full diagnostics of the business. Management must understand what the causes of distress are, the current situation and the realistic outlook of the business in a fact-based way.

This may seem as an obvious thing to do, but surprisingly many companies do not perform factual diagnostics. Often, they rather rely on their understanding of the company based on many years in the business and use this to suggest actions without having a full overview of the situation in a fact-based way. Such an approach will sometimes work, but it is a risky approach. More or less educated guesses may be wrong and recommendations insufficient.

By conducting thorough diagnostics, you reduce the risk and increase the chances of success. In a survey from 20131 of executives who had been in turnaround situations, only 22% said they performed diagnostics at the start of their turnaround programme. However, of the 22% of companies that performed diagnostics, 60% achieved a successful turnaround, whereas the success rate was only 34% among companies that did not perform diagnostics!

In conclusion, it is possible to do turnarounds without diagnostics, but it is much more likely that you will reach the desired destination if you start by checking where you are right now.

Acknowledging that there is a problem may be challenging and humbling

When you start out with turnaround management, the starting point is to acknowledge that there is a problem and objectively understand the severity of the problem. It can often be the case that existing management has played a big role in getting the company into trouble. Therefore, it can be very challenging and humbling to expect existing management to have an honest, objective and thorough view on the situation, as this may require them to admit to serious mistakes having been made.

Companies that have moved into a crisis over a long period of time might fail to see that they are in distress. Like a frog placed in water which is slowly brought to a boil, it is difficult to see danger that is building up slowly. In the previously mentioned survey, over half of the executives said they had either underestimated the severity of the problem or refused to accept that there was a problem at all2.

Delays in realising there is a problem can make the situation even worse. The faster you acknowledge that there is a problem, the more time you have to fix it before it gets worse. Even if management can be blind to own mistakes, it is important to take early warnings seriously. These early warnings can come in many forms.

We have made a non-exhaustive list of eight examples of “yellow warning flags” to watch out for:

- Increasing and rapid management turnover

- Large and increasing negative variances between actual performance and budgeted expectations

- Lenders tightening borrowing lines

- Increasing net working capital (through e.g. inventory build-up, increasing aging of receivables and increasing payables/late payment of invoices)

- Increasing quality problems and customer returns as well as postponement of major repairs

- Production problems (e.g. overcapacity, strikes, machine breakdowns etc.)

- Creative accounting practices and significant one-time adjustments

- Significant market downturn and/or new aggressive and successful competitors

It is important to note that these are not root causes but warning signals of something going very wrong. If and when one or more of these occur(s), ask yourself if you really know why it occurs and if you know the full extent of the problem. Can you honestly say that you are on top of the situation? Performing objective, data-driven diagnostics will help you “get on top of the situation”.

If you have ever tried to get rid of dandelions in the garden, you know that it is not enough to act on the symptoms. You must get to the root of the dandelions, or the problem will just keep reappearing.

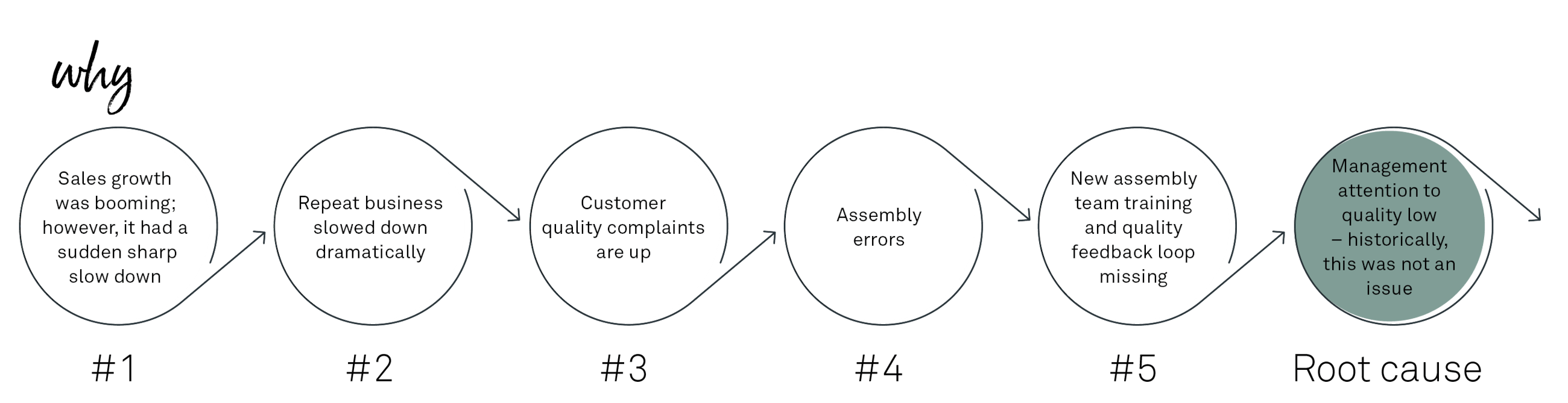

And the very issue of getting to the root cause is the basics of diagnostics. To find the root cause, it is important that you keep digging until you get down to the root. Here, you can use the “five whys”, a simple – but often overlooked – lean discipline/analysis technique with which you can move beyond symptoms by asking “why” until you reach the true root cause of an issue.

When you continue to ask why, you can and should find the actual reason for the issues at hand. For a real-life example, see figure 2.

Figure 2: A real-life example of the “five whys”

When conducting the root cause analysis, we recommend that you keep going until you get to a point where management could improve, as leadership is ultimately responsible for the direction of a company, and faults cannot and should not be “blamed elsewhere”. Ultimately, management needs to own the leadership.

A structured approach to diagnostic evaluation

Your diagnostics should give a preliminary viability analysis and determination of the nature of the turnaround, i.e. is the turnaround possible, and what are the key areas to work on?

The more distressed the situation is, the less time there is to analyse. However, we do not recommend skipping any of these areas. The more critical the situation is, we rather recommend shortening, speeding up or postponing some of them. One area not to skip is the cash flow. This step is crucial to understanding the current situation and the options going forward.

Here are 3 important steps in diagnosing the turnaround situation.

- Diagnosis 1: diagnostic evaluation - A fact-based understanding of the situation and potential combining the external and internal view of the company.

- Diagnosis 2: forward-looking cash flow - A realistic forward-looking cash flow projection highlighting the main sources and drainage of cash and the time horizon available with realistic best, likely and worst-case scenario options. The cash flow is the key tool to manage the whole targeting, planning and controlling of the implementation of the turnaround plan.

- Diagnosis 3: value creation priorities - An identification of the main levers of short-term value creation.

The forthcoming sections give a suggested guideline of what to investigate in a diagnostic evaluation.

As stated earlier, each turnaround situation is unique and will not require the same review. But taking time to understand what/where the problem lies is part of finding the solution and the way forward. However, only go deep where it makes the most sense. Do not fall into the trap of “boiling the ocean”. Performing diagnostics can also help to uncover many quick hits; capture and pursue these. Also, do not take too long with the diagnostics phase, and do not try to solve everything. Instead, move through this phase to the “value creation” design and impact phases with speed. And, ultimately, remember that the purpose of the diagnostic phase is to help you get an overview of the situation and help you prioritise where to focus your efforts to improve performance.

Diagnosis 1: diagnostic evaluation

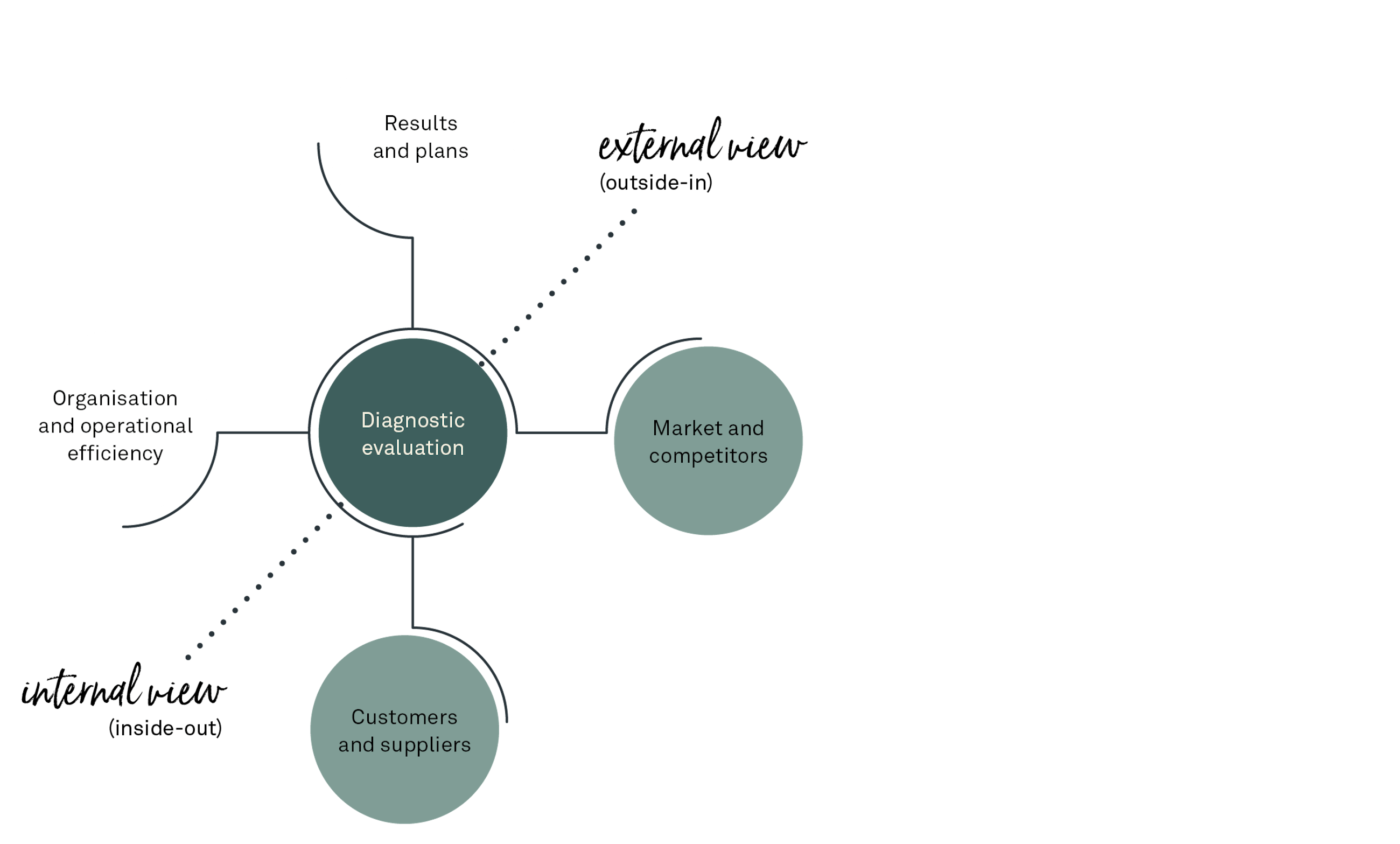

When performing a diagnostic evaluation, there are four important lenses to look through:

- Market and competitors

- Customers and suppliers

- Organisation and operational efficiency

- Results and plans

It is important that you get a fact-based understanding of the weaknesses of the company and the root causes of these. In many cases, the root causes are what needs to be fixed to get back on track.

But it is equally important that you understand the strengths of the company and if these can be leveraged more to compensate for the weaknesses.

You should review the strengths and weaknesses in an objective and – to the extent possible – data-driven way. You should use an internal as well as an external view of the company as visualised in figure 3.

Figure 3: Use an internal as well as an external view of the company

Looking through the external lenses, market and competitors are two areas to look into. It is fundamental to any business to be clear about the business definition. What is/are the target market(s) and the business boundaries, i.e. who are the target customers, is the business local, regional or global, and what are the competing products and services. If several businesses are involved, then the understanding of the interrelatedness of these businesses is important, and then for each business, the understanding of the health of that market as well as the strength of the competitive position and performance is important. What ultimately matters in performance is performance relative to market and competitors – and available cash flow.

No customers, no revenue – as simple as that. It is important to understand if customers are satisfied and loyal, and if not, why? Net promoter score or NPS can be a useful KPI for benchmarking. Understand the strengths and weaknesses of the products and/or services offered. In addition to customers, suppliers are also another important – but often forgotten – source of outside-in information about the performance of a turnaround company.

Below are some examples of questions to ask related to the external factors:

External view

Market and competitors | Customers and suppliers |

Market

| Customers

|

Competitors

| Suppliers

|

For the internal view, it is important to compare how well, or not, the company has performed compared to plans. The health and cash potential from sales, profitability, costs, net working capital (NWC) and assets is important to understand. Additionally, it is important to see how well the organisation is working as well as the operational efficiency. The organisational strength, management capabilities and organisational complexity are some of the aspects one can look into.

For an example of questions to ask related to the internal factors, see below.

Internal View

Results and plans | Organisation and operational efficiency |

Results

| Organisation

|

Plans

|

Operational efficiency

|

You can conduct a diagnostic scan by asking the right questions such as the ones listed here. After doing so, you highlight the main priority challenge(s) that need(s) urgent resolution.

Below, we present examples of real turnaround cases and the diagnostics they have performed.

Case A

A global logistics equipment manufacturer needed to stop profit leak. The sales units were struggling to turn the equipment installation business profitable. The gross margin for the units’ projects was very low and not sustainable and varied greatly from 2% to -47%. Some of the issues found were that prices were too low, and too many discounts were given. Prices were not realistic, as they did not cover late additions and changes. Sales had previously set prices on rough calculations and then not updated them, and engineering had not answered fast enough in the past. It all boiled down to understaffed engineering, breakdown in communication between sales and engineering, too complicated portfolio – too flexible with customers’ demands/too complicated offering. The solution included: improving project portfolio management in engineering, clearly defining a robust Stage-Gate quote-to-order process, improving communication and building a collaboration culture between engineering and sales and finally tools, CRM, training and coaching.

Case B

A construction equipment manufacturer experienced flat sales despite the fact that the market was booming. Diagnostics found that the product delivery was not competitive. Only 17% of deliveries to customers were on time, supplier on-time delivery to the factory was only at a level of 61%, and there were over 20 quality issues per product. The solution to boosting sales was therefore to dramatically improve the end-to-end supply chain. This resulted in increasing productivity, decreasing lead times, decreasing inventory value while increasing on-time delivery to customers – and ultimately a considerable lift in sales and profits.

Case C

A company within the specialised engineering sector found that their revenue had dropped in the last two years. At the same time, the overall market was expected to continue to grow. The company had a strong position within their global niche market, but the market was changing, and the competition was getting tougher with higher cost awareness. The company was mainly targeting capital expenditure design business and was not strong in follow-on operational services. A closer look at the customers suggested that even though they appreciated the high quality and technical capabilities, they did not want to pay the price anymore, as there were cheaper options. Furthermore, the company, being technically very strong, was not good at building long-term customer relationships and had high overall variability in customer satisfaction. After diagnostics, the key challenge was found to be that the traditional core business attractiveness was eroding, and there was a need to refocus the company to evolve new value-added services and become a lot more customer-oriented vs building on their traditional technical inward-looking core capabilities.

Diagnosis 2: forward-looking cash flow

At the end of the day, cash is the ruling monarch, as it is needed to pay suppliers and staff and to continue operations. Succeeding in turning the business around requires, as a minimum, positive cash flow generation (from operations and/or investors) in the short term to keep the business going and in the long term to generate value for shareholders.

Therefore, it is important that you understand the cash flow situation and projections. These should contain an operating cash flow, investing cash flow and financing cash flow to give a complete view. In your cash flow projections, you should include sensitivity scenarios based in part on realistic high, medium, low and worst-case market outlook scenarios as well as likely business scenarios.

At the end of the day, cash is the ruling monarch.

Many cash flow forecasts have annual or quarterly time forecasts in them. However, depending on the severity and urgency of the distress situation, it is important that you also have a short-term cash flow forecast with monthly, weekly and potentially even daily forecasts.

Why short-term cash flow forecasting? In rough waters, it is your early warning indicator and possibly an invaluable tool to stay afloat. In a steady state, it is the lifeblood of treasury operations. Moreover, it is also a critical business process that enables companies to make liquidity and short-term investment/borrowing decisions.

There are four simple questions that need to be addressed:

- How much cash do I have/will I have going forward?

- How much cash will I need?

- When will I need it?

- Where (and when) will I get it?

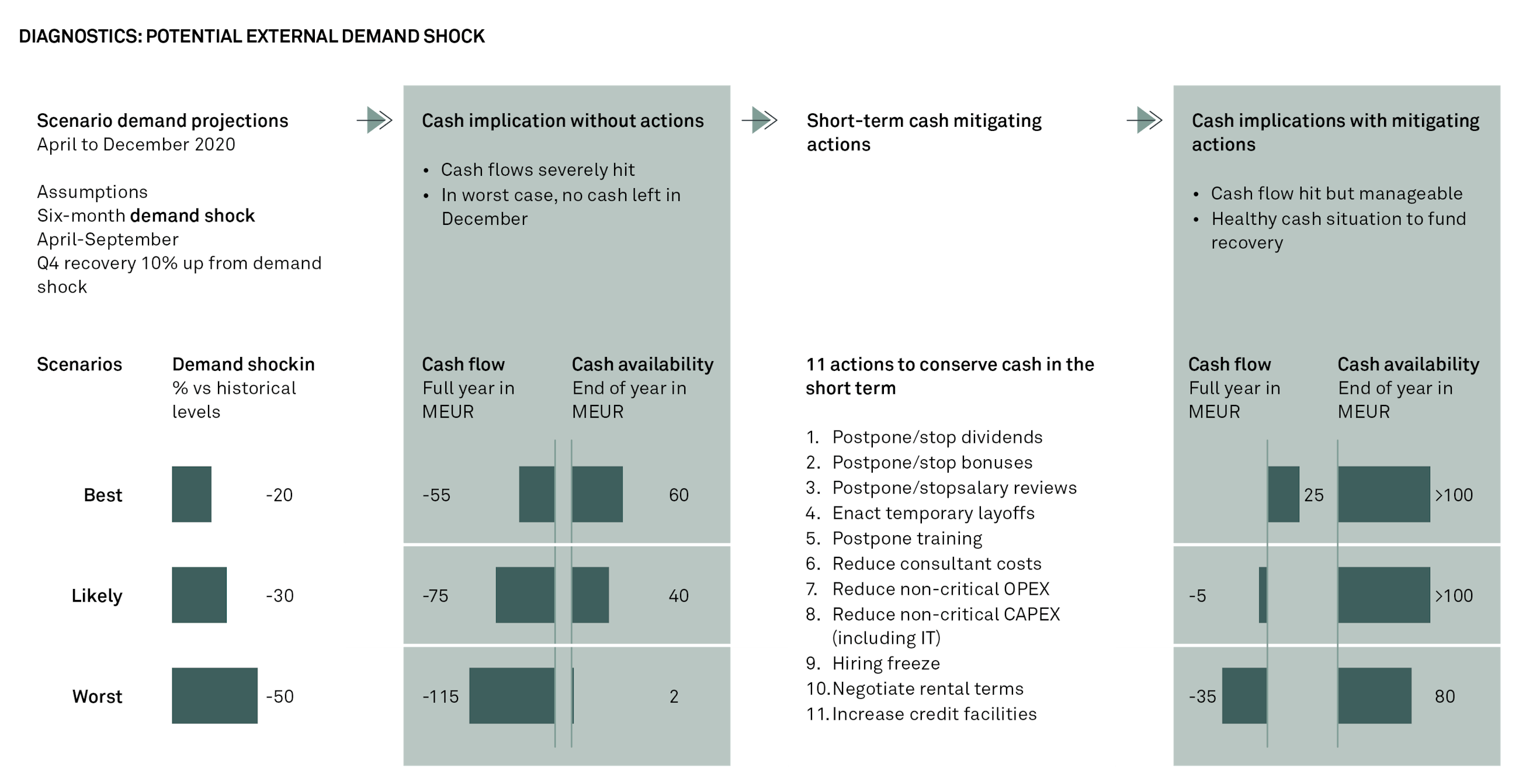

Below, there is an example of a company that was hit with a demand shock due to COVID-19, i.e. an external trigger for the turnaround. This required immediate action to preserve cash flow and cash availability.

Figure 4: An example of a company that was hit with a demand shock

The company did three scenario evaluations of the likely future demand outlook, i.e. best, likely and worst-case top line outlook. From this, the company forecasted the cash generation and cash availability under the assumption that no cash-conserving actions would be taken, and this indicated how much was required to do to conserve cash. On the basis of the forecast, the company decided on 11 actions to conserve cash and updated the consequential cash flow and cash availability scenarios. With that, they felt their actions were sufficient to weather the storm and be ready to redevelop the business from the new situation.

The short-term cash flow provides clarity on the liquidity situation, which is particularly crucial when managing a company in severe distress. It determines the path a restructuring can take and the options available.

There are six areas to consider with regard to short-term liquidity in a severe turnaround situation:

1. Creditors

- Is the company able to service interests?

- Does the company need to adjust financial commitments?

- Is there a need for fresh money?

2. New investors

- Is there a need or a possibility for new investors?

- (Discuss with current and new lenders).

- Are there any M&A sales options for parts or all of the business?

- Should the company seek out investors specialising in distressed situations?

3. Strategic plan

- Does the strategic plan, as it is set up and run, offer realistic options?

- Is there a need for a new plan?

4. Directors’ duties

- In a distress situation, what are the legal duties for management?

- (E.g. in terms of warning/informing banks and other stakeholders and writing down goodwill and assets etc…).

5. Set priorities

- How distressed is the situation?

- Is this a case of focusing 100% on liquidity preservation vs having more time to pursue performance improvement of the business?

6. Insolvency options

- How close is the company to insolvency?

- What is the “plan B” and downside of an insolvency scenario?

- Should the company file immediately?

- Is it possible to explore a “pre-packed” insolvency process?

Short-term liquidity is the core building block of any restructuring. Most of all, it gives you clarity on the urgency of the situation and the time available to explore options. It is best practice to start with a cash flow forecast, and it is often key to determine whether a company has the “right to fight” or is required to file for insolvency.

Diagnosis 3: value creation priorities

The final part of the diagnostics works as a bridge to the other parts of the turnaround toolkit. It is about the importance of prioritising efforts by using the knowledge you have gained about the situation through the previous steps.

No company or person can do everything, especially in a turnaround situation. Therefore, it is important that you prioritise what to focus on to fix the situation in the best way possible. As each turnaround situation is unique, so will the value creation priorities be.

As mentioned in the introductory article, there are four generic value creation levers:

- Net working capital reduction: reducing inventories and accounts receivables and increasing accounts payables.

- Cost reduction: reducing fixed and variable costs along the whole value chain.

- Sales value creation: optimising pricing, product and volumes profitably.

- Financial restructuring: securing needed financing as cheap and advantageous as possible and/or restructuring the business (e.g. closing or selling parts or all of the business).

You should look into all four areas. It is among, as well as within, these areas that the value creation priorities should be identified. When you make your priorities, it is important that you base them on the specific situation at hand and on the analysis and input gained about this from the diagnostics.

It may be difficult to select exactly which priorities are right, as future events inevitably will affect the optimal prioritisation. But it is still important that you start with a set of priorities, focus to improve performance within these and modify/improve them over time.

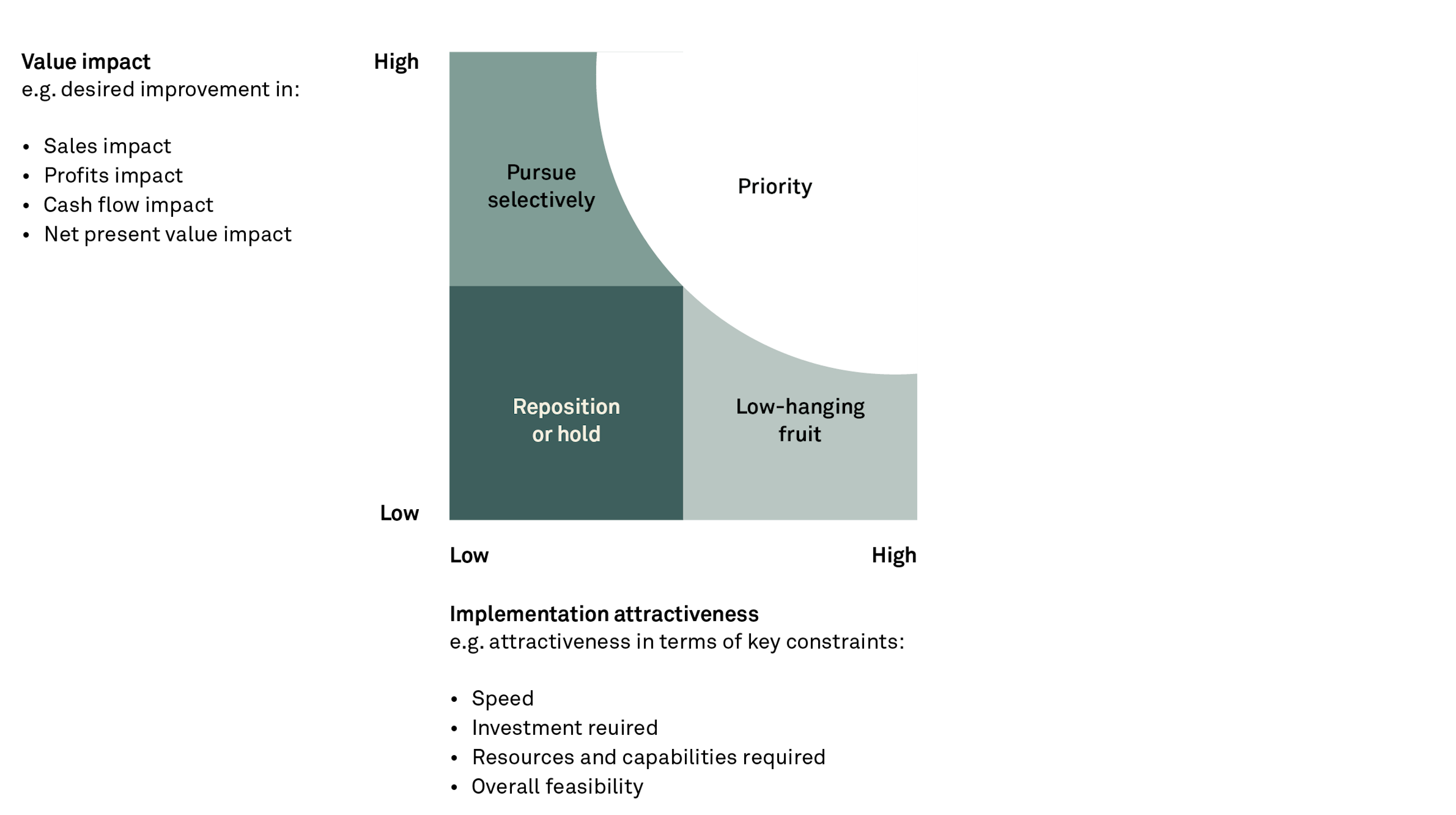

You should prioritise actions and projects based on their value impact and the implementation attractiveness with regard to what makes the turnaround situation critical, e.g. time, resources, capabilities, investor patience, cash etc.

The value impact can be analysed with different levels of depth or detail from sales and profitability improvement impact to full cash flow and net present value improvement impact. Also depending on the situation and degree of depth of analysis, “implemented attractiveness” can mean quickest and/or with the least amount of investment and/or implemented with existing resources and capabilities and/or implementation feasibility.

Figure 5: A prioritisation framework

You will get a helpful overview of the improvement programme if you map up the opportunities into a prioritisation framework. The opportunities with highest priority can be found in the upper right corner as seen in figure 5.

In turnaround situations, every little bit helps. This is why you should pursue opportunities with high implementation attractiveness even if their value impact is low. On the other hand, initiatives with high value impact but low implementation attractiveness need to be pursued selectively. In this case, the improvements are needed, but the company may not be able to muscle the requirements to implement them – this will be determined by the constraints at hand, e.g. how much cash is available. By implementing a high value impact opportunity, a company might be able to make room for more opportunities later on, as the first opportunities can buy time or generate cash for the company or in other ways enable additional opportunities to be pursued.

Looking at opportunities with low value impact that are also difficult to implement, you must investigate if these can be repositioned to higher value by e.g. bundling the ideas, or be easier to implement by e.g. de-complexing the ideas to give these opportunities more meaning to pursue – or simply putting them on hold.

Note that there may sometimes be opportunities and improvements that have little value impact and are difficult to do, but that are “key enablers” for value lift in a company. This may e.g. be a new product platform or a costly factory closure. While the financial positive value impact of these may be limited or even negative if they are a key to unlocking value in other related opportunities, then this must be considered and in a way valued to help repositioning them to ensure that they are prioritised to unlock the much needed value upside from the related initiatives.

The severity of the situation does have an impact on the priorities you choose. While some turnaround companies may be at the brink of bankruptcy where speedy and dramatic measures are required, other turnaround companies may be facing a situation of declining revenues or profitability but with sustainable cash flows and have more time and resources to turn the trend to a positive. Consequently, the turnaround situation has an impact on what value creation options to pursue. While turnarounds at the brink of bankruptcy will need to cut costs fast and ruthlessly, companies wanting to turn around declining performance but with strong cash flows will opt for focusing more on long-term impact priorities such as process improvements and product development investments to boost performance.

The turnaround situation has an impact on what value creation options to pursue.

In addition to considering the severity of the situation when you define your priorities, you must also consider at what stage you are in a turnaround.

The typical stages of a turnaround include:

- The management change stage

- The diagnostics stage

- The emergency stage (sometimes needs to come first if situation is critical)

- The stabilisation stages

- The “return to financial stability” stage

The later the stage, the longer you can work with your actions and plans.

Is it worth it?

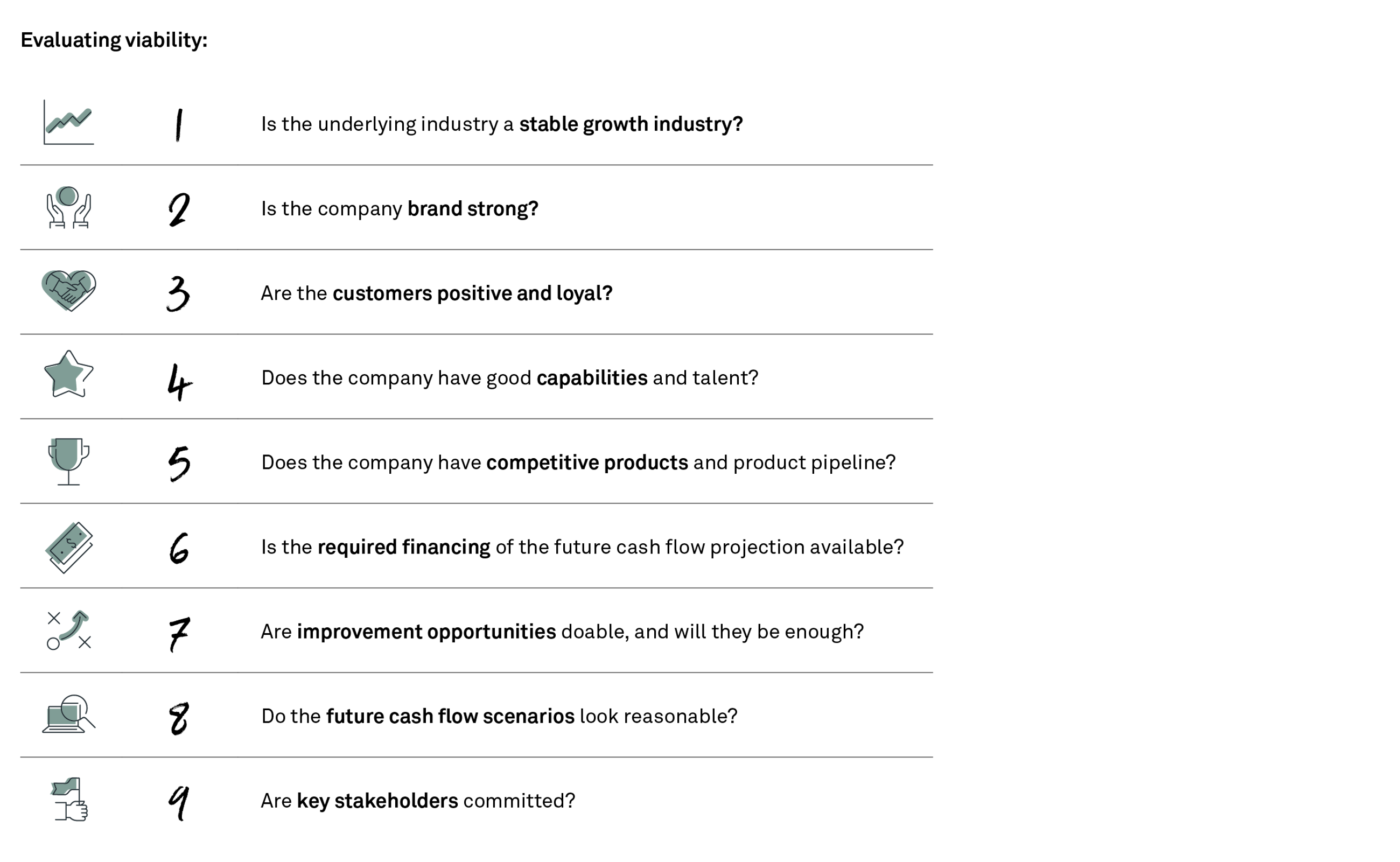

Working with turnarounds is hard work, and it is a good idea to check upfront if it is worth it. As we know, not all turnarounds are successful – in fact, some are not even possible, which is important to acknowledge as early as possible.

Turnaround viability depends on a number of supporting factors. Here are nine questions to consider when evaluating the viability:

Figure 6: Nine questions to consider when evaluating the viability

None of these factors alone can imply a firm conclusion of the viability of a turnaround. However, they help support the case.

Not all turnarounds are possible to perform, but if they are viable, they should start with diagnostics to improve the chance of success.

Sources

1 & 2 Breuer, P., Elmalem, T & Wigley, C. (2013/14). In need of a retail turnaround? How to know and what to do. McKinsey & Company Article in Perspectives on retail and consumer goods, Number 2, Winter 2013/14.

The McKinsey global survey on recovery and transformation was in the field from January 22 to February 1, 2013, and received responses from 1,527 executives representing the full range of regions, industries, company sizes, tenures, and functional specialties.