Article

Why reporting lines in finance are a strategic choice – not a default setting – that deserves more than a standard answer.

Article

Read more

8 April 2026

A finance strategy sets the direction. It defines the role finance will play, the value it will create, and the capabilities it needs to deliver. Translating that strategy into reality requires the design of a finance target operating model, which provides a blueprint for how finance is structured, governed, and operated.

Within the finance target operating model, one of the most consequential design choices is typically how to organise: where to place decision rights, how to balance global consistency with local responsiveness, and how to connect finance professionals to both the enterprise and the business they serve. Two often-overlooked strategic decisions in finance organisation design are how finance is anchored in the business and how reporting lines are set up.

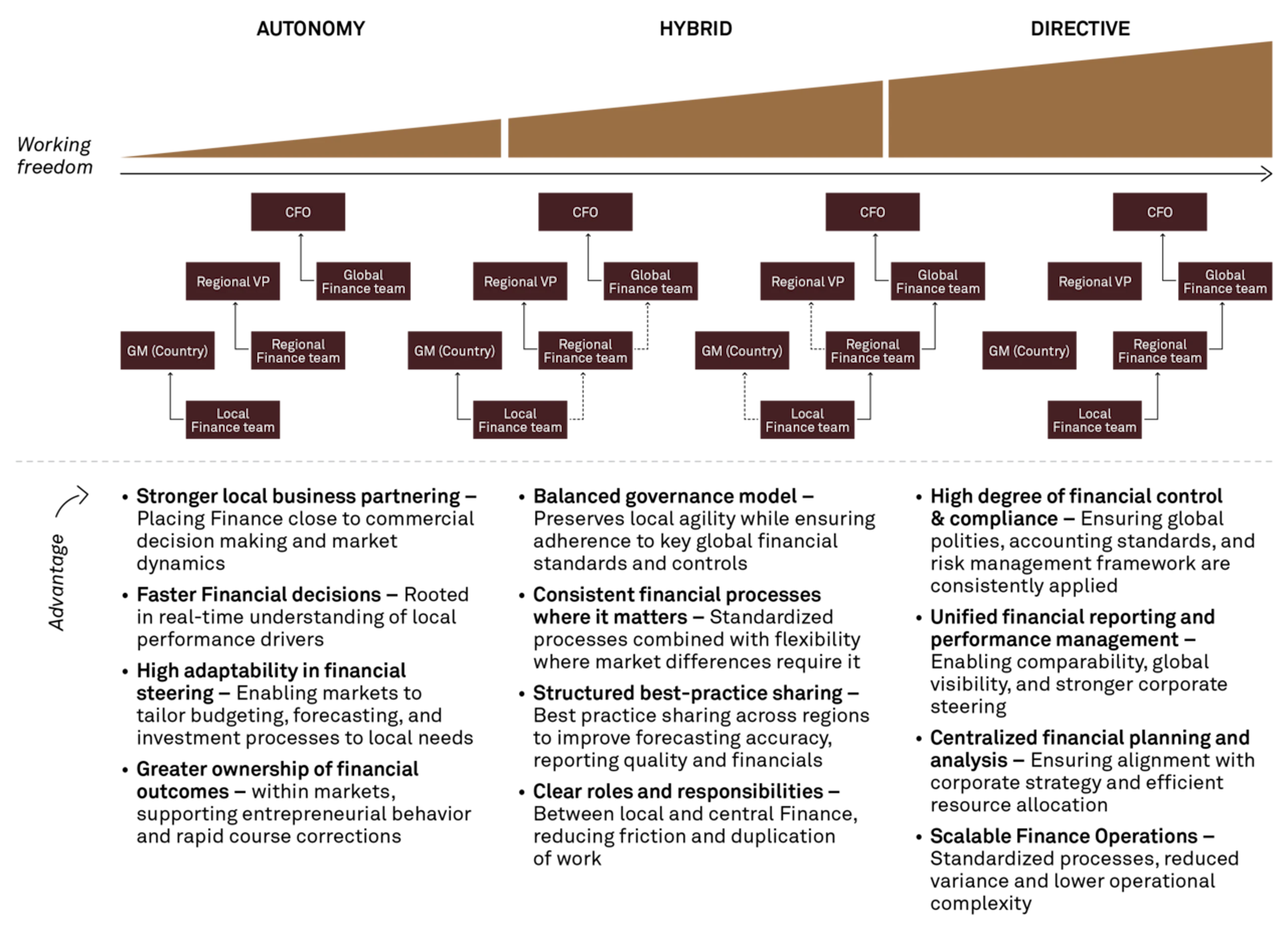

The way you structure reporting lines effectively defines finance’s role, either as a central partner to the enterprise (directive), an embedded advisor to markets (autonomy), or a blend of both (hybrid).

With that in mind, the key question is where on this spectrum your finance organisation should sit today and what shifts are needed over time to balance control, speed, and business partnership. Should finance have a directive global reporting line to the CFO? Should local finance leaders have more autonomy by reporting into the local General Manager, with a dotted line to the global finance organisation? Or does the answer, as it so often does in a hybrid model, lie somewhere in between?

In our work with CFOs and finance organisations, we frequently encounter a firmly held assumption that direct reporting lines are a prerequisite for a global, efficient, and high-performing finance function. This article challenges that assumption, not to argue that one model is inherently better, but to highlight that reporting lines are a strategic design choice with trade-offs, and that this design decision deserves the same deliberate attention as any other element of the operating model.

Many finance leaders view direct, global reporting lines to the CFO as foundational for a high-performing finance organisation. We call this the directive model. The logic is straightforward: by consolidating decision-making authority and aligning global and local teams under one chain of command, finance can move faster, standardise at scale, strengthen control environments, build talent, and reduce cost.

This setup is considered particularly effective when finance is expected to lead enterprise-wide process ownership, drive consistent data structures and systems, and deliver timely and trusted decision support across markets. The key drivers behind this view include:

Taken together, these drivers represent a compelling ‘inside-out’ perspective from the CFO’s viewpoint. However, this is not the only perspective worth considering, as it may disconnect finance from the needs and realities of the business, i.e. the ‘outside-in’ perspective.

An alternative view on reporting lines is gaining traction, driven by two distinct considerations. First, there are strategic benefits to having local reporting lines with a dotted line to global finance. Second, many of the advantages traditionally attributed to direct reporting can be achieved through other means without restructuring the reporting line itself.

The key advantages of local reporting lines include:

The argument is not that dotted-line benefits outweigh direct-line benefits in all cases. Rather, it is that many of the outcomes typically associated with the directive model – standardisation, control, governance, and talent development – can also be achieved through clear mandates, shared platforms, performance management, and a well-functioning finance community. So, while direct reporting lines are a sufficient condition for many of these outcomes, they may not always be a necessary one.

This paves the way for a strategic question: if the benefits of direct lines can be delivered through governance and operating model design, is it worth sacrificing the proximity and partnership that more local reporting lines provide?

There is no universally correct answer, and it may not be an either/or choice. Our experience is that the right reporting structure depends on the organisation’s strategy, industry, risk appetite, and maturity. Below, we outline five criteria to guide the decision.

It is also worth considering whether a single model should apply uniformly across all markets. In many organisations, less complex or strategically less critical markets may be better served by direct reporting lines to global finance, while commercially important or locally complex markets benefit from a stronger local presence. Existing local capabilities and budget considerations should naturally be factored into this assessment.

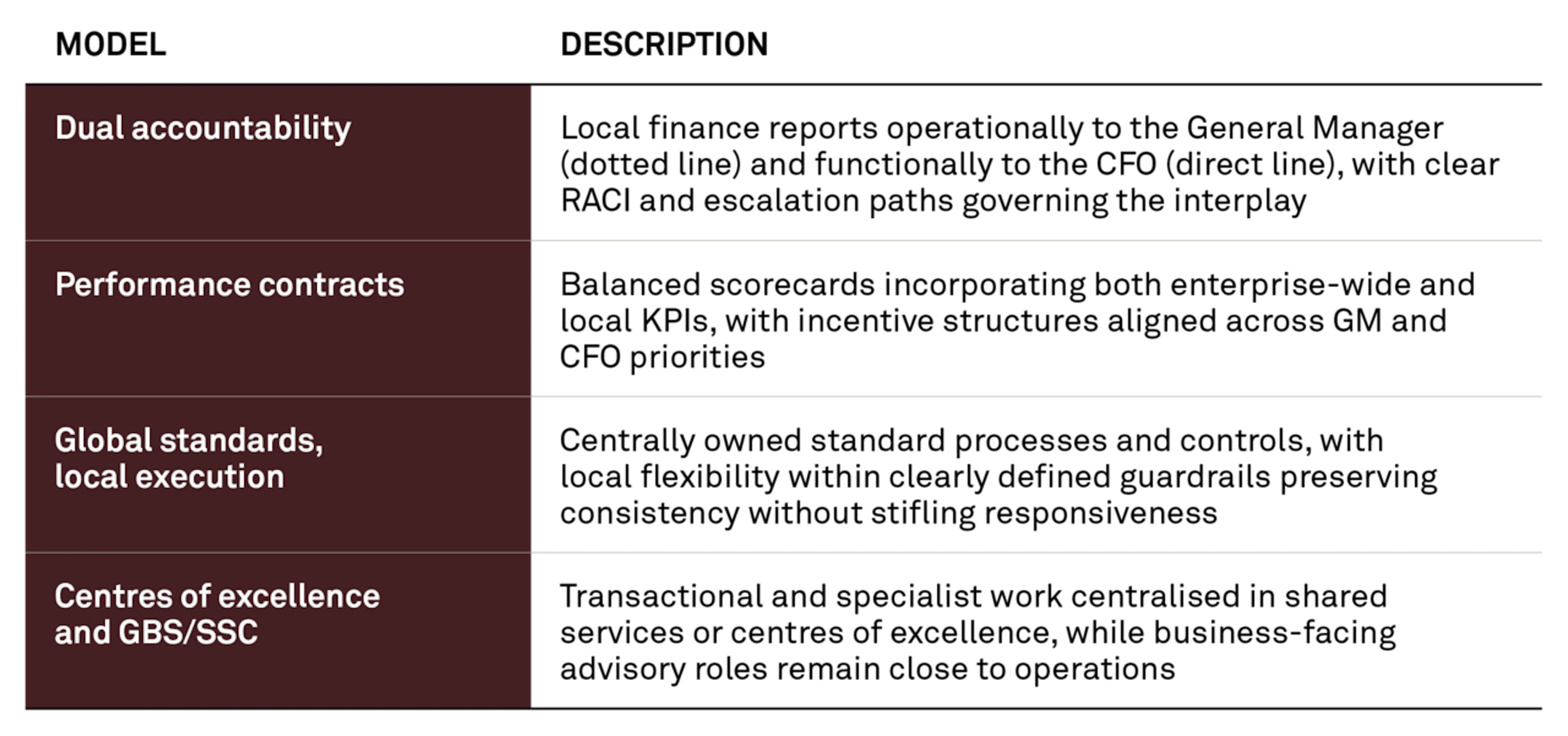

In practice, the choice is rarely binary. Several hybrid models exist that blend elements of direct and dotted reporting, each striking a balance of control, proximity, and integration.

Examples of these models include:

We work with CFOs and finance leadership teams to make deliberate, well-founded choices about reporting lines as part of a broader finance strategy and operating model design. Based on years of practical experience across industries and organisational setups, our approach centres on five steps:

The goal is not so much to identify the ‘correct’ reporting line model in the abstract, but to design a solution that is fit for purpose: one that supports your finance strategy, enables your operating model, and can evolve as your organisation matures.

This article is the first in a series on strategic finance operating model choices, with upcoming topics including finance business partners, shared services centralisation, and the impact of AI on finance function design.