Article

Published

5 May 2026

The AI landscape: traditional, generative, and agentic AI

Traditional artificial intelligence (AI) refers to machine learning and statistical models that operate on structured data to automate, predict, and optimise decision-making processes. These systems are designed to identify patterns and improve outcomes in areas such as forecasting, risk management, and operational efficiency.

Generative AI (GenAI) extends these capabilities by using large language models (LLMs) and other generative architectures that are built to handle general inputs and outputs. GenAI can analyse and create content from unstructured data such as text, images, or audio, enabling more interactive and context-aware use of information. An assistant (often used interchangeably with agent) is an LLM configured to perform a specific task through prompt engineering and data access.

Agentic AI systems equip LLMs with a level of autonomy and access to a predefined toolbox, allowing models to perform complex tasks such as writing code, drafting slides, querying databases, and accessing systems.

AI has proven its significant value by enabling us to better serve our customers, reduce response time, and deliver more accurate risk information. [It will] revolutionise our business model and pioneer the next generation of insurance solutions.Mario Greco, Chief Executive Officer, Zurich Insurance Group

The state of AI in commercial insurance and reinsurance

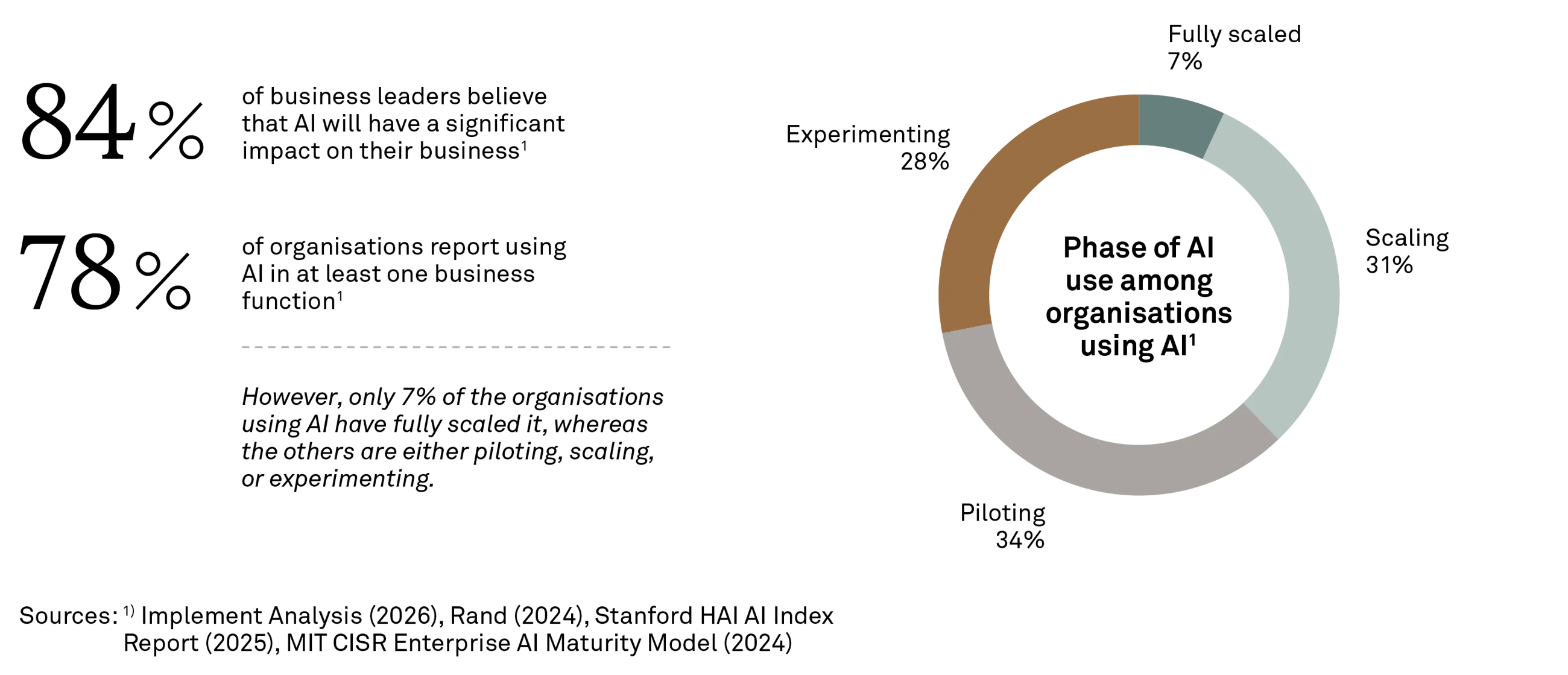

The insurance industry is undergoing a pronounced split in its approach to artificial intelligence. Large insurers have moved beyond proofs of concept and are now establishing dedicated AI hubs with a focus on enterprise-scale deployment. These organisations are investing heavily in scaling AI across claims, underwriting, and customer operations. Mid-tier players represent a sizable segment that is willing to commit budget, but they expect credible, implemented AI solutions rather than slide-based promises.

The impact areas for AI in insurance are across the entire value chain, with different levels of penetration. Cost reduction is the primary driver of adoption, with insurers seeking tangible efficiency gains, especially in claims handling time, underwriting throughput, and CX workload.

However, progress is tempered by persistent barriers: data quality and availability remain the single largest obstacle, closely followed by limited AI literacy across leadership teams, leaving decision-makers uncertain about where to start, what to prioritise, and how to execute effectively.

From a workforce perspective, the industry experts anticipate a slight net reduction in headcount over the next three years, accompanied by a significant reskilling effort. The shift is not towards wholesale automation but towards augmented decision-making; adjusters supported by AI-generated summaries, underwriters accelerated by document intelligence, and service agents complemented by conversational bots. The near-term trajectory is one of selective, evidence-driven adoption: scaling what works, proving value quickly, and investing in the foundational data and platform capabilities that make enterprise AI viable.

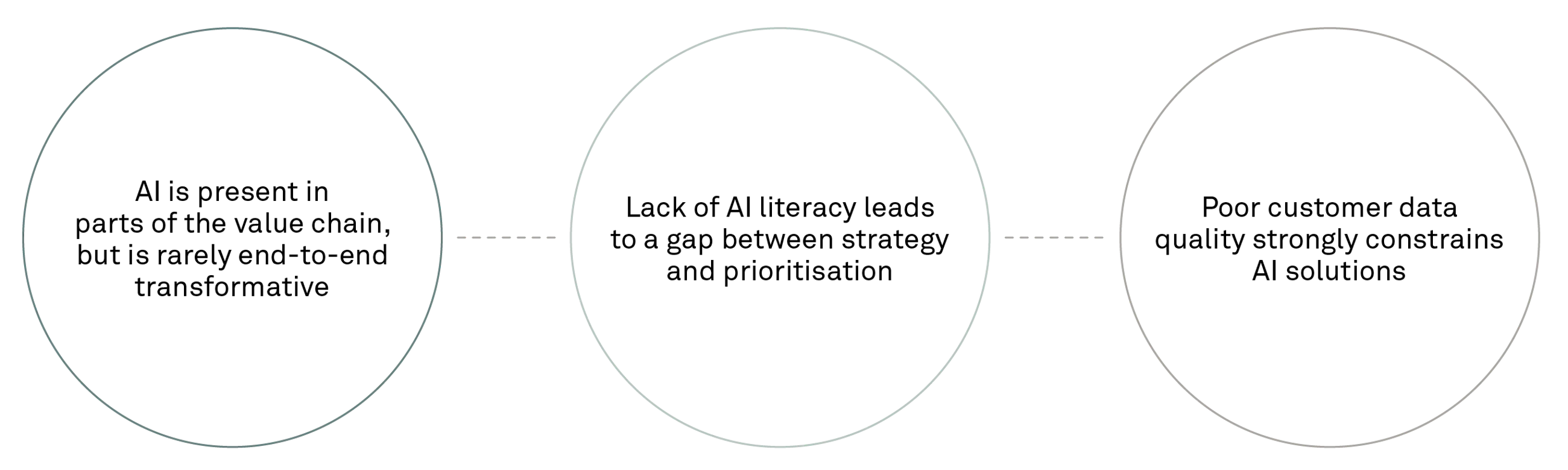

Research indicates that insurers are ahead in some parts of the value chain, but systematic adoption remains uneven

Current state of AI adoption in commercial insurance and reinsurance …

AI maturity in insurance varies across the value chain, as is the case in many industries. Claims processing and customer service represent the most advanced areas, with agent-assist tools and chatbots already deployed or in active scaling. Pricing and underwriting are transitioning from traditional ML models to more sophisticated document AI and dynamic pricing engines.

Core platform vendors are embedding AI features directly into their products, lowering the barrier to AI adoption within existing workflows.

The industry is past the proof-of-concept phase among large carriers but far from enterprise-wide AI integration.

… so, what is hindering adoption?

Our research finds that uncertainty about where to start is slowing adoption. The generality of the technology provides a wealth of opportunities but having the right people to prioritise and plan AI initiatives proves crucial to success.

Another identified barrier is fragmented, low-quality customer data. Duplicates, inconsistent naming, and scattered profiles prevent a reliable customer master, undermining personalisation, cross-sell opportunities, and claims analytics. Without robust entity resolution and data cleanup, even strong models yield unreliable results, yet these foundational efforts remain under-invested.

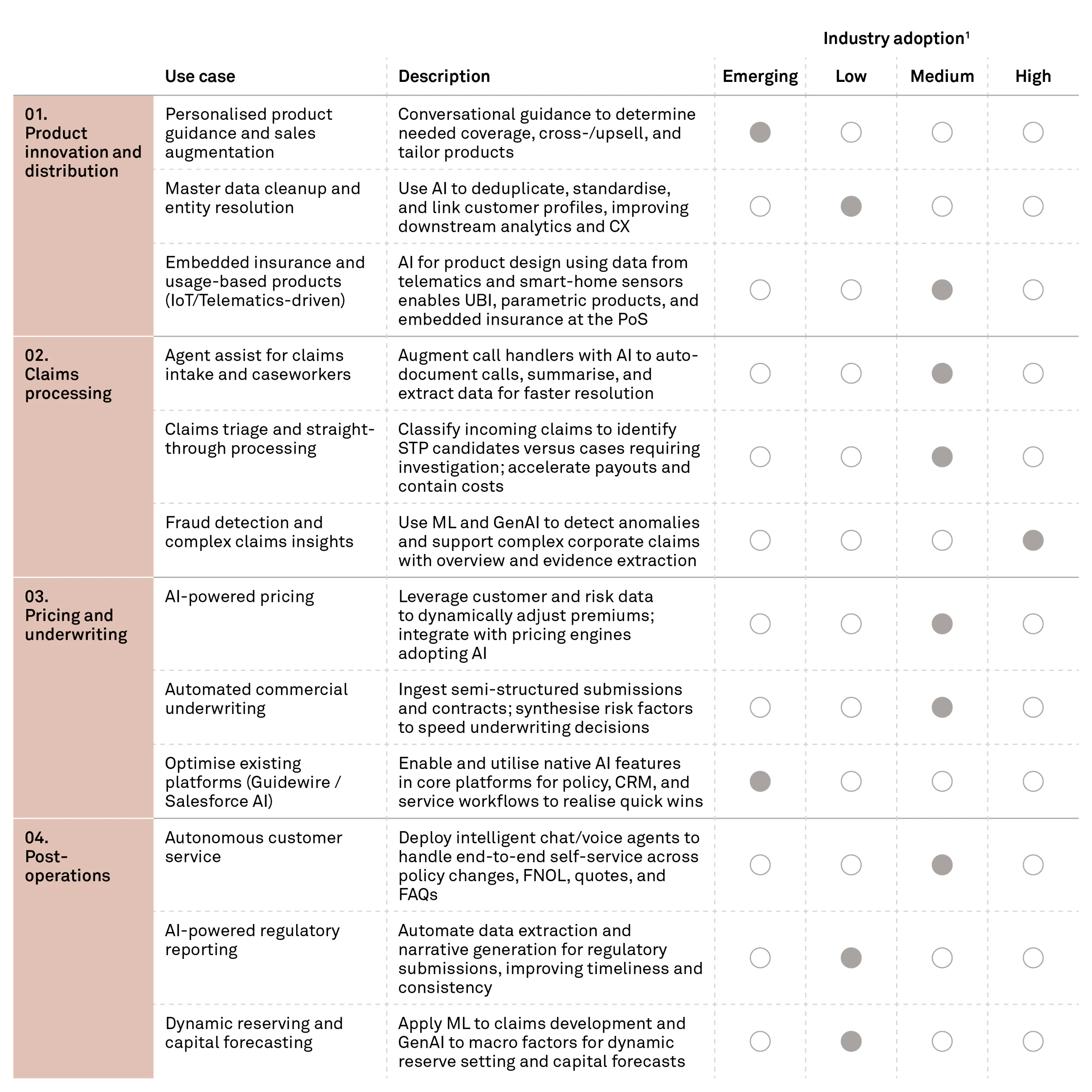

AI across the value chain of insurance and reinsurance

AI is already transforming insurance operations and services, creating competitive advantages for early adopters.

Highlighted AI use cases in insurance

Several advanced AI use cases are implemented at full industrial scale and can deliver significant returns on investment from day one.

AI reference case

Implement Consulting Group use case

This case demonstrates how moving beyond legacy processes and adopting an AI-first mindset can unlock meaningful impact.

State-of-the-art agentic AI solution with potential to fully automate service requests

Customer operations // Agentic AI

A client sought to move beyond static FAQs and manual service handling by deploying an autonomous, agentic AI solution. Implement Consulting Group supported the client in designing and deploying a decentralised agent architecture where specialised AI agents collaborate directly to resolve complex queries in real time. The solution enables low-latency, personalised responses while establishing a scalable foundation for future voice-enabled interfaces and internal productivity workflows.

Impact

- Enabled low-latency resolution of complex service requests, including during peak demand

- Delivered personalised responses leveraging live core system data

- Established a scalable foundation for 24/7 automated service operations

In our experience, insurers must make explicit strategic choices to unlock the value of AI

There are no universally 'right' answers – but there is a cost to not making the choices explicit. Realising sustained AI impact is driven by a small number of deliberate strategic trade-offs.

In our experience, insurers must make explicit strategic choices to unlock the value of AI – deep dive

From potential to value

How do we translate AI capabilities into sustained customer and shareholder value?

There is no universally right answer. In fact, there is not even a single right question. Insurers are instead faced with a set of interdependent strategic choices that must be navigated over time. Each choice involves trade‑offs. Not choosing is also a choice, often with a tangible cost. Together, these choices form the foundation of an organisation’s AI strategy.

These considerations are rarely best addressed as a linear sequence. They are better understood as a ‘choice cascade’, where decisions in one area shape what is realistic in others. Many AI initiatives stall, not because the technology is immature, but because underlying choices are not formally made, leaving the organisation in a state of uncertainty.

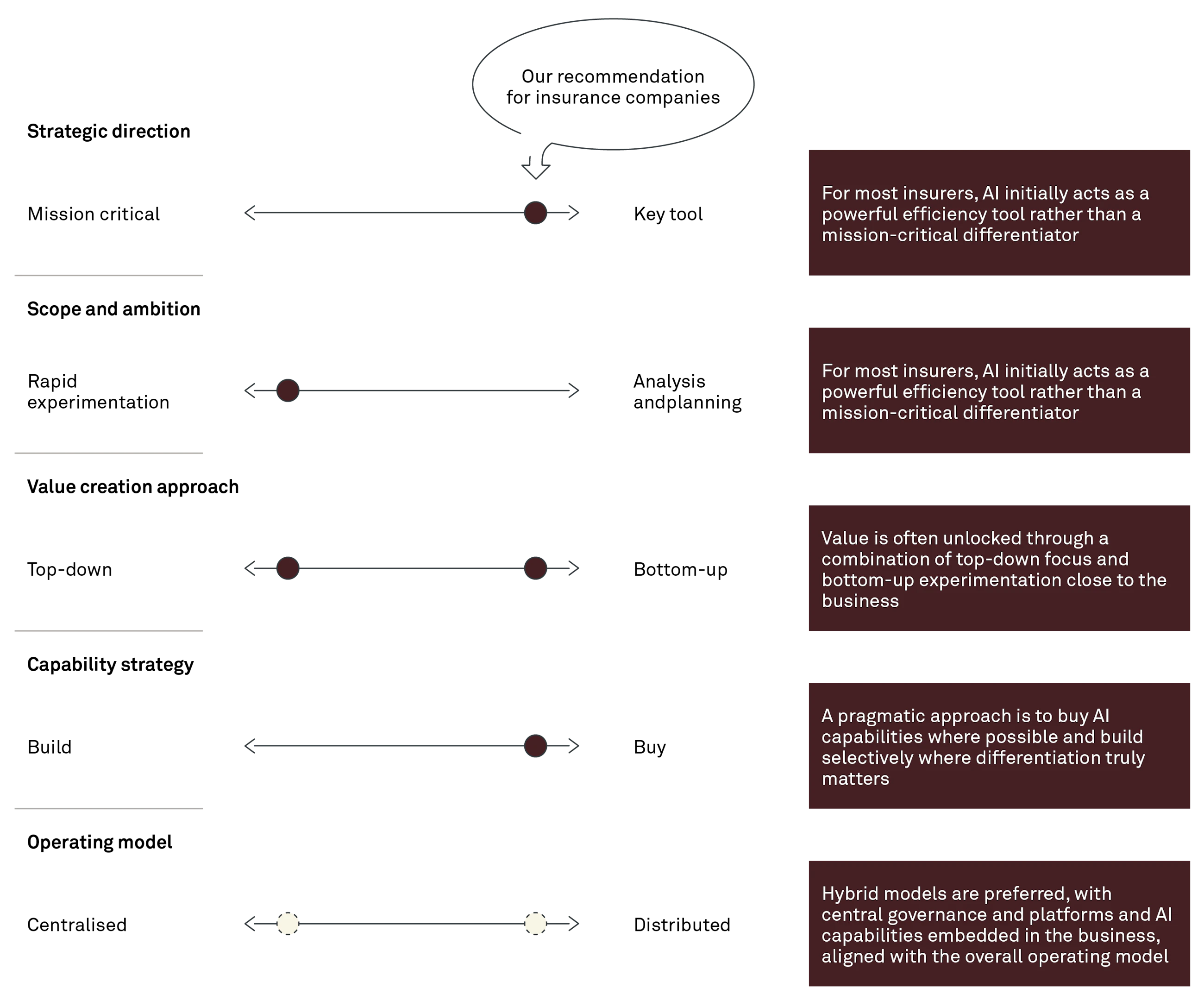

Strategic direction

An AI strategy, like any divisional strategy, should enable the organisation’s overall strategic direction. A central consideration is whether AI is viewed as mission-critical to long‑term competitiveness, or primarily as a powerful tool to improve and optimise existing operations.

When AI is considered mission-critical, organisations typically accept longer investment horizons and greater uncertainty in return for potential long‑term advantage.

When AI is viewed primarily as a tool, investments tend to be more cautious and closely tied to near‑term business cases and measurable returns. Timing matters as well. Some insurers expect AI to become mission critical over time, while remaining a useful optimisation lever in the short to medium term.

In our experience, most insurance companies today lean towards this latter position. AI is often approached as an efficiency and productivity lever first. This can be a sensible starting point, provided the choice is explicit and revisited as technology and competitive dynamics evolve. Strategy is as much about choosing what not to pursue as it is about selecting where to invest.

Scope and ambition

One of the most practical challenges in any AI strategy is deciding how to identify opportunity areas to pursue. Many insurers balance between rapid experimentation on the one hand and more deliberate analysis and planning on the other.

Rapid experimentation can accelerate learning and quickly surface opportunities with high business impact. At the same time, without clear oversight and coordination, it risks leading to fragmented initiatives with limited scalability. Analysis and planning provide structure and coherence but can slow learning in a fast‑moving field if taken too far.

For most insurers, the question is not which approach is right, but how to combine them. The aim is to enable experimentation within a clearly defined scope, while ensuring that successful initiatives can be industrialised and scaled.

Value creation

Closely linked to scope and ambition is how specific AI use cases are identified. A top‑down approach, where leadership defines focus areas, can work well where problems and outcomes are relatively well understood. A bottom‑up approach, where teams are empowered to explore new applications, can support adoption and uncover new value.

Each approach has strengths and limitations. In practice, insurers that are currently focusing on using AI as an efficiency and productivity lever tend to lean towards a top-down approach. However, all insurers are likely to benefit from a deliberate combination of approaches, aligned with their ambition and maturity.

Capability strategy

Once priorities are clearer, the question of build versus buy becomes pertinent. Off‑the‑shelf solutions typically offer faster time to value at lower cost, but with limited differentiation. Custom solutions offer greater control and potential for competitive advantage, but require sustained investment and ongoing ownership.

A pragmatic stance for many insurers is to always buy where possible and build selectively where off‑the‑shelf solutions are not viable, particularly close to the core of the business, where competitive advantage matter more. Given the pace of AI development, patience can sometimes be as important as speed.

When AI becomes part of everyday operations rather than a parallel structure, value realisation becomes more likely.

Operating model

Regardless of sourcing choices, AI capability will be developed in-house. That capability can be centralised or distributed across the organisation. Centralised models support scale, consistency, and governance. Distributed models support business relevance and adoption but are often harder to scale.

As a result, many insurers move towards hybrid models, with central governance and platforms combined with AI capabilities embedded in the business. The optimal hybrid is often where the AI operating model aligns with how the organisation already runs the business.

A concluding thought for leadership teams

Despite significant investment, few organisations have yet demonstrated sustained bottom‑line impact from AI. Ironically, this is pushing many organisations towards rapid time to market initiatives often with more promising short-term ROIs – in turn limiting longer term scalability and operational efficiency.

Realising sustained AI impact is driven by a small number of deliberate strategic trade‑offs, rather than isolated technology investments.

Future outlook

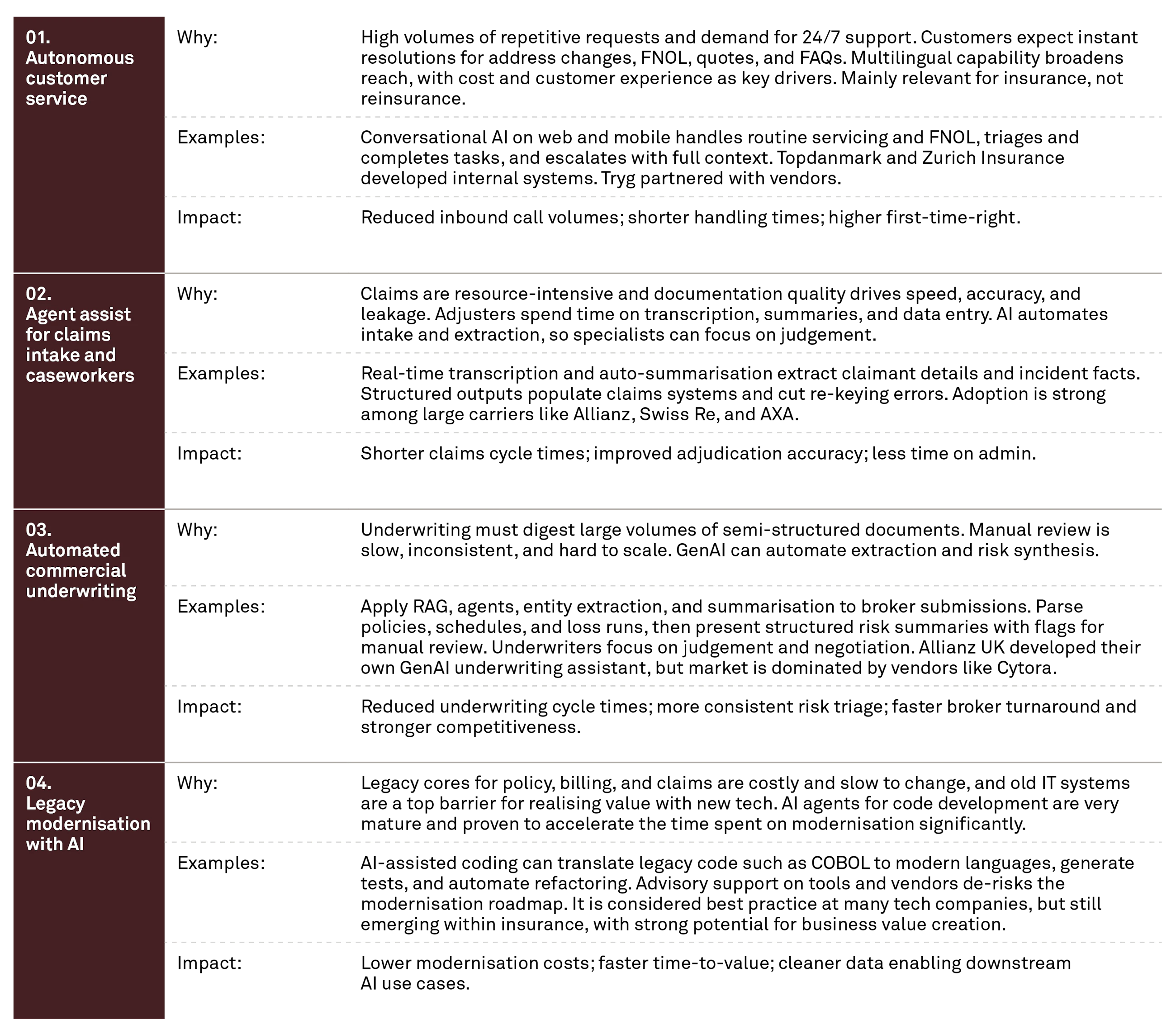

Across industries, including insurance, organisations are moving in a common direction. Not because the destination is known, but because standing still is no longer an option. The early leaders are not those with perfect roadmaps, but those who take AI seriously, invest early, and remain curious and experimental.

In the near term, insurers are scaling customer service automation and claims agent assist with proven ROI while activating native AI in core platforms with Azure, Google suite, Guidewire, and Salesforce to capture quick wins with minimal integration. Over the medium term, focus shifts to underwriting and pricing, with GenAI streamlining commercial submissions and improving risk triage, and dynamic pricing engines maturing as richer, real-time data is integrated.

The hard work lies inside the organisation. Technology matters, but the real challenge is understanding where AI can fundamentally reshape value creation across the organisation and value chain, and where experimentation, not optimisation, is required.

At Implement, we see early leaders investing not just in technology, but in AI factories, data foundations, assurance, and, most importantly, organisational learning. Societal adoption will influence how AI evolves, but lasting impact will depend on organisations’ ability to disrupt themselves from the inside out.

Reach out to our experts0 4

0

4Related0 4

Article

Read more

CFO Advisory #2: Lead finance through the uncomfortable middle

Set the direction. Design the approach. Protect the capacity to learn.Article

Read more